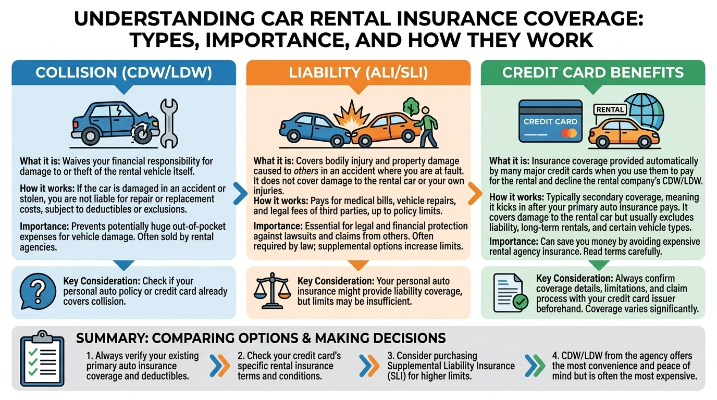

Understanding Car Rental Insurance Coverage

Insurance

|

May 12, 2026

When planning a trip or embarking on a long drive, one essential detail often overlooked is whether your car insurance covers rental vehicles. Every unexpected event can quickly turn a delightful getaway into a financial headache; grasping the nuances of car rental insurance is vital. Picture this: returning from a long-awaited vacation, only to be confronted with steep repair bills from a rental car accident. This situation, without proper knowledge of your insurance coverage, could leave you liable for significant expenses that your existing policy might have shielded you from.

When planning a trip or embarking on a long drive, one essential detail often overlooked is whether your car insurance covers rental vehicles. Every unexpected event can quickly turn a delightful getaway into a financial headache; grasping the nuances of car rental insurance is vital. Picture this: returning from a long-awaited vacation, only to be confronted with steep repair bills from a rental car accident. This situation, without proper knowledge of your insurance coverage, could leave you liable for significant expenses that your existing policy might have shielded you from.

Understanding if your current auto insurance includes coverage for rental cars is not merely a question of peace of mind—it's about making well-informed choices that protect both your finances and legal standing. This article will explore the key factors influencing your coverage, dispel common misconceptions that could lead to costly mistakes, and provide practical tips to help you navigate the available options. By the time you finish reading, you will have a better understanding of how your car insurance influences your rental car experience, enabling you to make savvy driving decisions during your next adventure.

Why Is Covering Rental Cars Important?

Having rental coverage is essential for drivers, especially when considering the potential financial implications of accidents or damage incurred while renting a vehicle. Without adequate insurance, a minor incident can lead to substantial out-of-pocket expenses. For instance, if a driver rents a car and finds themselves in an accident, the rental car company could hold them responsible for any repair costs, which can rise rapidly; what seems like a simple fender bender could easily lead to repair bills exceeding $1,000—an amount many may not be ready to pay without insurance before them.

Additionally, the legal liabilities associated with renting a vehicle further underscore the importance of having rental coverage. If a rental car gets into a collision causing injury to another person, the driver could face lawsuits and hefty claims. Lacking sufficient coverage could put individual financial stability and even personal assets at risk. Risk management while traveling is a necessity, as unforeseen events can strike at any moment. For example, imagine a tourist renting a car for a road trip, only to realize that they are liable for damages resulting from an unfortunate mishap. Proper rental coverage not only provides tranquility but also acts as a financial safeguard against potentially devastating incidents. In essence, comprehending rental car insurance is not just about protecting a vehicle; it’s about securing your financial and legal well-being during travel.

Factors That Affect Rental Car Insurance Coverage

Several elements can determine whether your personal auto insurance policy extends coverage to rental cars. Generally speaking, most personal auto policies provide insurance for rental vehicles if they include coverage for your own car. However, nuances can vary considerably among insurance carriers.

Collision Coverage: This type of coverage typically extends to rental cars as it would to your personal vehicle, provided you have collision coverage on your auto policy. In the event of an accident, this can help protect you from out-of-pocket expenses related to damages.

Liability Coverage: Liability insurance generally applies when driving a rental vehicle. However, limits might differ compared to your personal vehicle coverage, making it vitally important to verify specifics with your insurer.

Credit Card Benefits: Many credit cards feature primary or secondary rental car insurance, which may overlap with your personal policy. Nonetheless, there may be exclusions, especially if the rental is used for business instead of leisure.

Other Influencing Factors: The type of vehicle rented, duration of the rental, and geographic location can also affect coverage. Luxury or exotic vehicles might necessitate additional coverage, while shorter rental terms could offer automatic coverage.

10 Proven Ways to Reduce Rental Car Insurance Costs and Avoid Coverage Gaps

Compare Insurance Policies for Rental Coverage

Not all rental car insurance policies are created equally, making it crucial to compare coverage options from various insurance companies. This diligence helps in both identifying the most favorable deals and ensuring adequate protection. While some insurers may boast lower premiums, it’s imperative to investigate the specifics of what each policy covers. For example, one provider might include "loss of use" coverage—compensating the rental company for lost income while the vehicle is out of commission—while another might not include this benefit. Keep an eye out for each provider's deductibles and claim processes, as these terms and conditions can vary significantly. By comparing policies, you can make an informed choice that safeguards your finances and enhances your rental experience, ultimately saving you money on rental car expenditures.

Check Your Collision Coverage Rental Car Benefits

Collision coverage is vital when renting a vehicle since it covers damages to the rental car caused by an accident. Before securing a rental, it's crucial to determine if your personal auto insurance provides collision coverage for rented cars. Consider this scenario: John rents a car during his vacation, believing all his auto insurance benefits apply equally. When he is in an accident, he discovers his collision coverage does not extend to rental vehicles, leaving him responsible for covering repairs. To prevent unexpected financial pitfalls, it's wise to review your policy details or directly contact your insurer for clarity before you rent, ensuring you're fully covered and avoiding undue expenses.

Understand Liability Coverage Rental Cars Requirements

Understanding liability coverage is fundamental when renting a vehicle. Most rental companies mandate a minimum amount of liability protection to guard against bodily injury or property damage that may result from an accident. These specifications can differ by location and rental agency, so it is crucial to read the rental agreement and clarify any uncertainties. For instance, should your personal policy lack adequate liability coverage, you may need to purchase supplementary protection from the rental agency. By investing time in research and asking pertinent questions, you can ensure compliance and shield yourself from possible financial losses should an accident occur.

Use Credit Card Rental Insurance Wisely

Many credit cards come with rental car insurance as a valued perk, potentially saving you money on additional rental insurance. However, to get the most from this benefit, it is vital to comprehend the nature of the coverage included. Certain credit cards only offer protection for damages to the rented vehicle, frequently excluding liability or personal injury coverage. Furthermore, you typically need to pay for the rental with the card in question to qualify for this benefit. Relying solely on your credit card’s coverage without thoroughly checking the terms could leave you inadequately protected should an accident arise. Always scrutinize your credit card’s terms to make sure you utilize the offered rental coverage effectively and elevate your overall rental experience.

Avoid Buying Duplicate Rental Car Insurance

When renting a vehicle, purchasing duplicate insurance can lead to unnecessary expenses. Many drivers are unaware that their existing auto insurance and certain credit card benefits provide sufficient coverage. Always take the time to assess your current insurance policies before accepting optional insurance offered by the rental company. For instance, if your personal auto insurance includes comprehensive and collision coverage for rentals, you may not need the rental company’s collision damage waiver, meaning you could be paying for coverage you already possess. Being well-informed and adopting a strategic approach to your insurance can help you avoid such financial burdens and make rental costs more manageable.

Increase Deductible Strategically

Increasing your deductible can be a straightforward method to lower your rental car insurance costs. Generally, opting for a higher deductible leads to reduced monthly premiums, allowing you to save money at the outset on rental insurance. However, it's essential to approach this strategy cautiously. For example, consider increasing your deductible to $1,000; ensure you have sufficient funds available to cover this amount should you face damages. Calculate your potential savings and evaluate whether this trade-off is sensible in your case. By taking a strategic approach to increasing your deductible, you can strike a balance between your budget and necessary coverage, yielding long-term insurance savings.

Ask About Rental Car Coverage Extensions

Don’t hesitate to inquire about coverage extensions from your insurance provider. Many times, adding extra coverage could be beneficial in specific scenarios like long-term rentals or when driving in unfamiliar territories. Engaging in dialogue with your insurer about these possible extensions can safeguard you further and minimize your exposure to potential liabilities. For example, if you plan to embark on an adventurous road trip, ensuring that your policy encompasses risks associated with travel, such as hazards or damages not covered by basic policies, will provide peace of mind. Proactively engaging with your insurer can unveil essential coverage extensions that can cater to your rental situation.

Document Vehicle Condition Before Driving

Before taking possession of a rental vehicle, documenting its condition is paramount. Take photographs and record any pre-existing damage to protect yourself against potential disputes later. If you return the car and the rental company claims you inflicted the damage, having this documentation can serve as clear proof of the car's state when you took it out. For instance, when Jane returned her rental car, she discovered a scratch; fortunately, she had documented that it was pre-existing, sparing her from unjust charges. This simple precaution can shield you from unwarranted liabilities and prevent additional costs down the road.

Review Personal Auto Insurance Rental Cars Terms

It's beneficial to regularly examine your personal auto insurance policy regarding rental cars. Insurance terms can evolve, and being informed about your current terms ensures you won’t face unexpected limits when the need arises. For instance, if your insurer modifies the agreement and restricts coverage on rentals, being unaware of this could be detrimental when renting. Habitually checking your policy details, ideally every six months or during renewal periods, helps ensure that your rental car coverage remains sufficient, effectively saving you from potential challenges and expenses in the future.

Consider Standalone Rental Car Insurance When Needed

Certain situations may call for the purchase of standalone rental car insurance for extra peace of mind. If you find yourself traveling internationally or renting a high-value vehicle, your personal insurance might not provide adequate coverage. Should your auto policy exclude specific vehicles or destinations, a standalone policy can fill these gaps and offer enhanced protection tailored to your needs. Carefully assess your risk tolerance along with your travel plans to determine whether this additional insurance is prudent, ensuring you embark on your journey well-protected and less stressed.

Confirm Coverage for International Rentals

When planning to rent a vehicle in a foreign country, verifying your insurance coverage specifics cannot be understated. Many standard domestic policies do not extend coverage abroad, potentially exposing you to substantial liabilities. Before traveling, review both your car insurance and credit card benefits to understand international coverage boundaries and exclusions to avoid unexpected issues. For instance, certain countries impose specific coverage requirements that your standard policy may not include. Ensuring you're adequately informed will help you navigate international car rentals with greater ease.

Avoid High-Risk Vehicle Classes in Rentals

Selecting high-risk vehicle classifications can significantly influence both your insurance costs and liabilities. Exotic cars, SUVs, or trucks often attract higher premiums due to the increased likelihood of substantial damage during accidents. When booking a rental, opting for more standard or economy vehicles not only tends to minimize liability risks but also benefits your wallet by yielding lower overall costs. Such choices not only provide financial relief but also foster a more relaxed driving experience, allowing you to concentrate on enjoying the road ahead while minimizing potential liabilities.

Common Mistakes to Avoid

Many drivers inadvertently make costly errors in the realm of rental car insurance that can result in financial burdens and legal complications. Here are some typical pitfalls to watch for:

- Assuming Full Personal Coverage Applies: Many wrongly believe their personal auto insurance comprehensively covers rental cars without acknowledging specific limits and exclusions. Always confirm coverage details with your insurer.

- Ignoring Credit Card Coverage Details: While certain credit cards offer rental car insurance, not all are included. Moreover, the coverage may come with conditions and restrictions. Review your card’s benefits closely before proceeding with a rental.

- Declining Insurance Without Checking Your Policy: Some drivers hastily decline rental insurance without verifying their current policy. Always check your insurance to ensure you have adequate protection in place.

- Overlooking Liability Coverage: Neglecting to account for rental companies' liability coverage can expose you to significant risk should an accident happen.

- Not Reading the Fine Print: Rental agreements can be intricate. Failing to read the fine print could lead to missed information regarding insurance policies and fees, leading to potential liabilities.

To avert these mistakes, take the necessary time to review your current insurance policy, investigate your coverage options, and familiarize yourself with the terms of rental agreements. Knowledge stands as a powerful tool to help you make informed decisions and mitigate risks when renting a vehicle.

When Should You Review or Change Your Policy?

Reviewing your auto insurance policy is a crucial step during significant life events. If you plan regular travel, it's wise to reevaluate your coverage, as extended time away might expose you to risks not accounted for in your current policy. This is particularly pertinent when renting a vehicle while traveling.

Acquiring a new vehicle is another turning point. If your new vehicle holds a higher value or includes advanced safety features, you may need to adjust your policy accordingly to correspond with its value.

Moving to a different state can also affect your insurance coverage, given the variations in regulations. It's essential to ensure compliance with local laws and that your policy meets the state’s minimum requirements.

Other life moments, such as marriage or adding a teenage driver, may necessitate a policy review to align with your changing coverage needs and optimize savings. Regular assessments ensure that you always possess the necessary level of protection to meet your current situation.

Was this helpful? Share your thoughts